What are Structured Settlements? How Do They Work?

Are you considering selling your structured settlement payments for a lump sum of cash? Read on to learn about the benefits, risks, and processes of selling your structured settlement payments with Liberty Settlement Funding.

Structured Settlement Payments: A Comprehensive Guide part 1

What are Structured Settlements, and How Do They Work

Are you receiving monthly or periodic payments from a Structured Settlement? or have heard those singing “Need Cash Now” & “It’s My Money And I Want It Now” commercials and wonder what they are talking about? Our goal with this blog is to provide clear and straightforward explanations of structured annuity settlements, covering their definition, how they work, and the types of cases in which they are commonly used.

How Does a Structured Settlement Work?

A structured settlement is a financial agreement that gives you money over time instead of all at once.

They are a payment arrangement compensating a person who has suffered an injury or illness resulting in financial damages. The settlement is typically a series of payments made over time rather than a single lump sum payment. These payments are intended to provide the injured party with continuous financial support.

A settlement agreement is reached between the parties involved when a settlement is established. This agreement outlines the terms of the settlement, including the amount of money to be paid, the duration of the payments, and any other conditions that need to be met.

In a structured settlement, the payments are made over a period of time and are typically set up through an annuity. An annuity is an investment vehicle that generates a guaranteed income stream and is usually purchased from an insurance company.

The insurance company invests the funds from the settlement. The agreed-upon payments are then made to the recipient according to the payment schedule. Several insurance companies issue payments for structured annuity settlements, including MetLife, Prudential, AIG, Berkshire Hathaway, and Allianz.

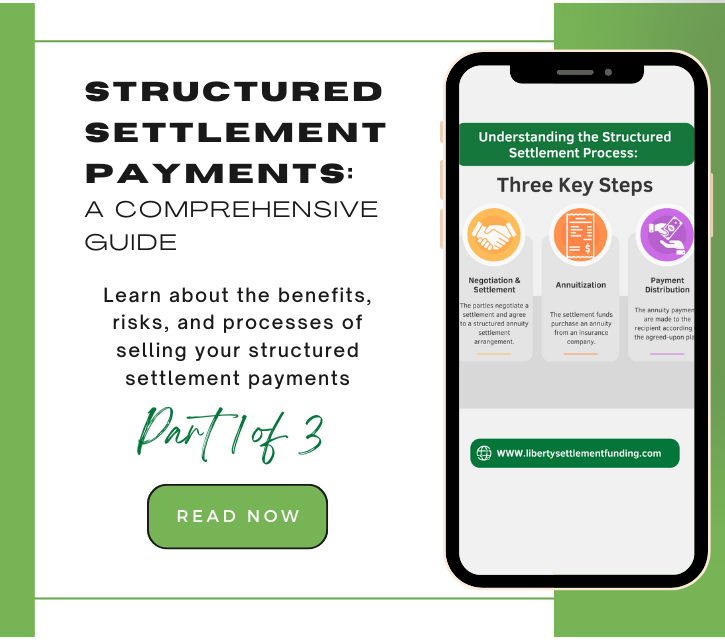

Three steps of the Structured Settlement Process:

Negotiation and Settlement:The parties negotiate a settlement and agree to a structured annuity settlement arrangement.

Annuitization:The settlement funds purchase an annuity from an insurance company.

Payment Distribution:The annuity payments are made to the recipient according to the agreed-upon plan.

A structured settlement is a payment plan that can be set up after receiving legal compensation, where you receive payments over time instead of all at once.

They are typically the result of a legal settlement or court decision. For example, suppose you are involved in a personal injury lawsuit. In that case, the other party may offer to settle the case with a structured settlement. Alternatively, a judge may order a structured settlement as part of a court settlement.

Once a structured settlement is established, the terms are outlined in a legal agreement between the parties involved. This agreement typically includes the amount of the compensation, the payment schedule, and other terms and conditions.

Why do you get a Structured Settlement – Top 5 facts, statistics, and trends

More than 35% of structured settlements are used to compensate victims of automobile accidents. (Source: National Structured Settlements Trade Association)

Approximately 40% of structured settlements involve medical malpractice or negligence cases. (Source: National Structured Settlements Trade Association)

More than 90% of structured settlements involve cases settled out of court rather than going to trial. (Source: National Structured Settlements Trade Association)

The number of structured settlements has steadily increased in recent years, with the value of structured settlements reaching approximately $6.4 billion in 2019. (Source: National Structured Settlements Trade Association)

About 15% of structured settlements involve cases related to workplace injuries or illnesses and may include payments for lost wages and medical expenses. (Source: National Structured Settlements Trade Association)

What types of cases are more likely to result in structured settlements?

Cases involving personal injury, medical malpractice, or wrongful death are often resolved through periodic payments.

They are often used in cases involving personal injury or wrongful death, medical malpractice, and product liability. They may also be used in workers’ compensation and employment disputes.

Periodic payments are prevalent in personal injury cases where the plaintiff has suffered a long-term or permanent injury.

However, they may not be appropriate in all cases. In some situations, a lump-sum payment may be a better option.

How do you get a Structured Settlement?

Structured settlements are often used in cases where a person has suffered long-term damage, such as medical malpractice, defective products, or workplace accidents.

They are typically set up through a legal settlement or court decision, particularly in cases involving personal injury, medical malpractice, or wrongful death. Rather than receiving a single lump sum payment upfront, the plaintiff agrees to receive regular payments over time.

The process of negotiating a settlement involves the plaintiff and the defendant (or their insurance company) working together to determine the terms of the settlement agreement. In addition, the parties will typically consult attorneys, financial advisors, and annuity companies to help structure the payments.

Once the terms are agreed upon, the settlement agreement is signed, and the payments are typically made through an annuity. The annuity is purchased by the defendant or their insurer.

How many people receive structured settlements?

According to the National Structured Settlements Trade Association, there are approximately 37,000 recipients in the United States annually. This number includes individuals who receive structured settlements due to personal injury lawsuits, medical malpractice cases, wrongful death lawsuits, and other legal proceedings.

History of Structured Settlements in the United States

Structured settlements were first introduced in the American legal system in the 1970s to provide long-term financial stability to individuals who had suffered personal injuries.

They have been a part of the legal system since the 1970s when they were introduced as an option to replace one-time lump sum payments in personal injury cases. They gained popularity in providing long-term financial stability and security to individuals who had suffered life-changing injuries or disabilities.

Today, they are used in many cases, including personal injury, medical malpractice, and wrongful death. The payments are typically set up through an annuity purchased from an insurance company. Liberty Settlement Funding specializes in helping individuals looking to sell their annuity payments for a lump sum of cash.

Structured Settlement Protection Acts

The Structured Settlement Protection Acts are important laws that help to ensure that individuals who have experienced a traumatic event and received a settlement are treated fairly and protected from exploitation.

The Structured Settlement Protection Acts (SSPA’s) are laws regulating structured settlement sales. They are designed to protect the rights of the payee and ensure that any sale of a structured annuity settlement is fair and in the best interest of the payee.

Under the SSPA’s, sales to a structured settlement company must be approved by a judge in the state where the payee resides or where the original settlement was made. The payee may also be required to receive independent professional advice before the court makes a decision.

The SSPA’s which vary state by state may provide several types of protections for payees: mandatory waiting periods before a sale can be finalized; a right to cancel the sale within a certain timeframe; and / or requirements for the disclosure of fees and costs associated with the sale.

In short, SSPA’s are a critical piece of legislation that protect the rights of structured settlement payees and ensures that sales of an annuity settlement structure that fall under the SSPA are fair and transparent and that when payees receive a structured settlement payout, they are treated fairly.

At Liberty Settlement Funding, we understand the complexities of purchasing structured settlements and annuities and can help you navigate the process.

Whether you’re considering selling your entire settlement or just a portion of your future payments, our team of experts can offer the information and guidance necessary to help you make an informed decision. Contact us today to learn more about our lump sum funding options and how you can sell structured settlements.